Bonds in a world of inflation risks and yield expectations

Emerging markets and local currencies as investment opportunity in 2026?

Investors are currently facing a number of challenges, particularly on the bond markets. Despite lower key-lending rates, long-term yields have recently started to rise again.

This situation raises a number of questions:

- Are US Treasury bonds still a safe haven asset, or have they become more of a political pawn and bargaining chip in the context of international geopolitical tensions?

- Is the debt momentum of developed countries still sustainable in the long run?

- Are the days of high inflation over, or should we brace for a return to at least more volatile conditions?

These are questions that bond investors need to ask themselves. In our view, one answer is to take a closer look at strong international diversification. There are arguments in favour of strategic allocation to emerging markets asset classes, even in the longer term; but also from a shorter, tactical perspective, there are a number of reasons to invest more heavily in these markets. Please note: investing in securities involves risks as well as opportunities.

Emerging markets bonds with attractive yields

This asset class has broadened considerably in recent years – both in terms of available volume and opportunities for diversification across countries, corporate issuers, and instruments. It now constitutes an institutionalised investment opportunity. Yields remain attractive at present.

Many central banks in emerging markets were taking a very proactive approach during the last inflation cycle. Key-lending rates were raised earlier than in developed markets, which then made it possible to cut them sharply again in a positive inflationary environment. Said environment remains supportive in many emerging markets, which is why in many cases their real yields are attractive.

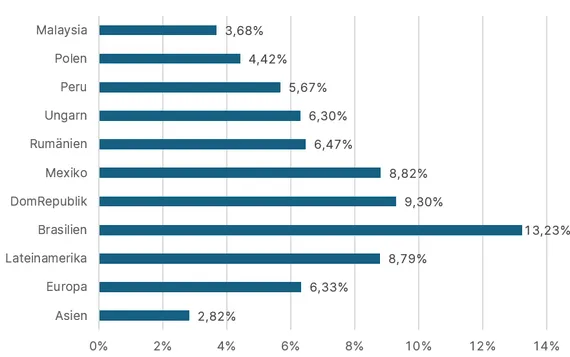

Emerging markets government bond yields in local currency

Source: Refinitiv Datastream, as of 28/01/2026

Growth advantage vis-à-vis developed economies

This asset class is quite diverse: Latin and South American countries could face a more liberal economic environment after the next elections. Many countries are benefiting from increased demand for commodities due to the global technology and infrastructure boom. In Asia, export dependence on the United States appears to be declining somewhat, and trade with other partners is gaining in importance. China, which is even exporting deflation, is providing additional impetus on the inflation front. These cyclical factors are giving many emerging markets a growth advantage over developed countries. This long-term trend is also leading to ever-improving credit quality, meaning that the structure of the asset class has changed significantly over the years.

Local currencies undervalued according to purchasing power parity (PPP)

In the currency sector, many countries have had to contend with the strength of the US dollar for many years. However, the market structure towards local currencies has helped to greatly mitigate the negative effects of such developments. The rising interest burden in the case of a strong US dollar relative to the local currency thus has a much smaller impact. The current debate about the US dollar as an international reserve currency and the questioned independence of the US Federal Reserve is affecting many emerging market currencies that are undervalued in terms of purchasing power parity.

Mercosur et al.: reorganisation of international trade

At the same time, a reorganisation of international trade flows is clearly a possibility. The best example at the moment is probably Mercosur, but other trade relationships are also sure to be reassessed in the near future. The relatively conservative fiscal policy coupled with low debt levels compared to various industrialised countries is ensuring a further positive rating trend.

In addition, quantitative factors are also at play in a multi-asset context: the volatility of emerging market currencies has declined. The asset class in all its forms, with an ever-widening market for corporate bonds, is no longer a niche market. The diversification effects that continue to exist also argue in favour of allocation to these markets.

In summary, given the challenges in the bond sector, there is little choice but to focus intensively on further diversification into international markets.

“Financial markets are like good cuisine: variety creates enjoyment. That's why it can make sense to refine familiar US burgers with a little Mexican chilli and Thai tom kha gai – or, in economic terms, to add emerging markets bonds to the mix.”

Gerhard Beulig, Senior Professional Fund Manager with Erste Asset Management

(c) Samuel Kreuz

Fund portrait: ERSTE RESPONSIBLE BOND EM LOCAL

ERSTE RESPONSIBLE BOND EM LOCAL is an actively managed bond fund that offers institutional investors broadly diversified access to emerging markets bonds in local currency. The fund invests primarily in bonds from supranational issuers and development banks, complemented by an assortment of government bonds from emerging markets. The regional focus includes Central and Eastern Europe, Asia, Latin America, and Africa.

The investment process follows a holistic ESG approach, in which environmental, social, and governance factors are an integral part of the security selection process. All securities must be classified as sustainable in accordance with a predefined sustainability process.

The fund's objective is to generate attractive current income and long-term capital growth. For investors who want to participate in the structural growth of emerging markets while taking sustainability criteria into account, the fund offers professionally managed access to a high-yield, yet challenging asset class. Please note: investing in this fund involves risks as well as opportunities.

For explanations of technical terms, please visit our Fund Glossary.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. Unless indicated otherwise, source: Erste Asset Management GmbH. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011. The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the web site www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the web site www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.